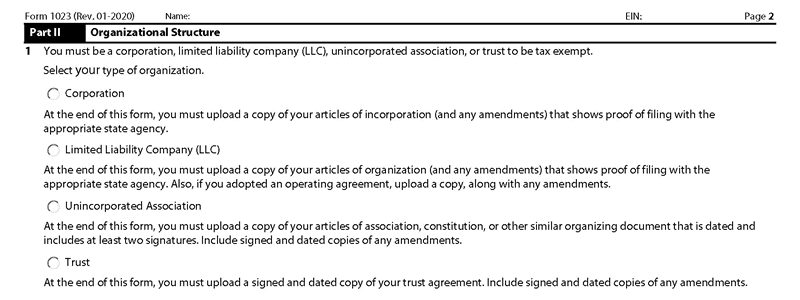

Form 1023 organizational structure, Corporation, LLC, or Unincorporated Association?

In Form 1023 Part II (2), the IRS tries to identify you as an eligible tax exempt organization. The phrase “organization” alone doesn’t mean anything to the IRS. A group of cats in the alley meowing can be called an organization, but not a legal entity. The IRS wants to know if you are a legally recognized corporation, unincorporated association, or trust.

Alright. I know many of you think that calling your entity an “organization” makes it sound more nonprofit-y than “corporation,” but legally speaking, these terms are not interchangeable, they are like eggs and pineapples. You need to call it what it actually is.

To file Form 1023 and get tax exemption, your nonprofit must be a corporation, an unincorporated association, or a trust.

Nearly every state requires nonprofits to incorporate under a specific designation, and you must file your Nonprofit Articles of Incorporation to be recognized as a Public Charity. Never incorporate as an LLC or other entity type if you want 501(c)(3) status – it makes it harder or impossible for no good reason.

Have you adopted bylaws?

If “Yes,” at the end of this form, upload a current copy showing the date of adoption.

In Form 1023 Part II, Question 4, you must answer YES. You need to adopt bylaws to show how you run your nonprofit organization. IRS might accept a written explanation, but this explanation is your bylaws (well sort of).

If you don’t adopt proper nonprofit bylaws, your application will almost certainly be denied. So do it right the first time. Don’t waste time with random bylaws downloaded elsewhere, throw them in the trash where they belong – use my bylaws template and thank me later. See the Nonprofit Bylaws page for how to write them right.

Are you a successor to another organization?

At the start of these articles, I made it crystal clear: I don’t help people who’ve dabbled in for-profit schemes before jumping to nonprofit to game the system by evading taxes. If that’s you, save us both the time and bugger off.

Saying that, if you are a nonprofit that’s a successor to a for-profit by mistake, and not claiming exemption for prior periods, you can just apply normally. In this case, you qualify for tax exemption as an organization described in section 501(c)(4) for the period beginning with the date you were legally formed and ending with the date you are recognized under section 501(c)(3). Generally, contributions made to a section 501(c)(4) organization are not tax deductible.

If you’re a successor to another organization, you have to complete the Form 1023 schedule G. Please visit this page for more information.

(Next Step) Instructions For Form 1023 Part III – Required Provisions

(Previous Step) Instructions For Form 1023 Part I – Identification Of Applicant

NOTE: If you’d like to receive the following organizing documents:

NOTE: If you’d like to receive the following organizing documents:- Nonprofit Articles of Incorporation,

- Nonprofit Bylaws,

- Nonprofit Conflict of Interest Policy,

- Conflict of Interest Policy Acknowledgment,

- Form 1023 Attachment with all the answers,

- Form 1023 Expedite Letter template,

- and Donor Contribution Form

in Microsoft Word Document format, please consider making a donation and you’ll get to download them immediately. Not only they're worth well over $1000 in value, they will save you weeks of copy pasting and formatting as they are ready to go templates which only need changing names and addresses.